Home Insurance in Arizona differs by $952 between the cheapest and most expensive premiums

By: Ramu Garuda July.19, 2019

A Gavop analysis finds that home insurance prices in the state of Arizona varies by 95% across cities, with the lowest premiums ranging between $996 in cities such as Sedona and $ 1,948 in and around Benson. The Insurance Information Institute (III) suggests that homeowners in Arizona spend an average of $803 per annum.

Nationwide offers the cheapest homeowners insurance premium in Arizona with an average premium of $798 per annum. Farmers, on the other hand, provides the most expensive homeowners insurance at a premium of $2,056 per annum.

Phoenix, the largest city in Arizona, reports an average homeowners insurance premium of $1,453, which is considerably higher than the state and national averages. Nationwide offers the cheapest homeowners insurance premium at $876 per annum, whereas Farmers has the highest average at $2,235.

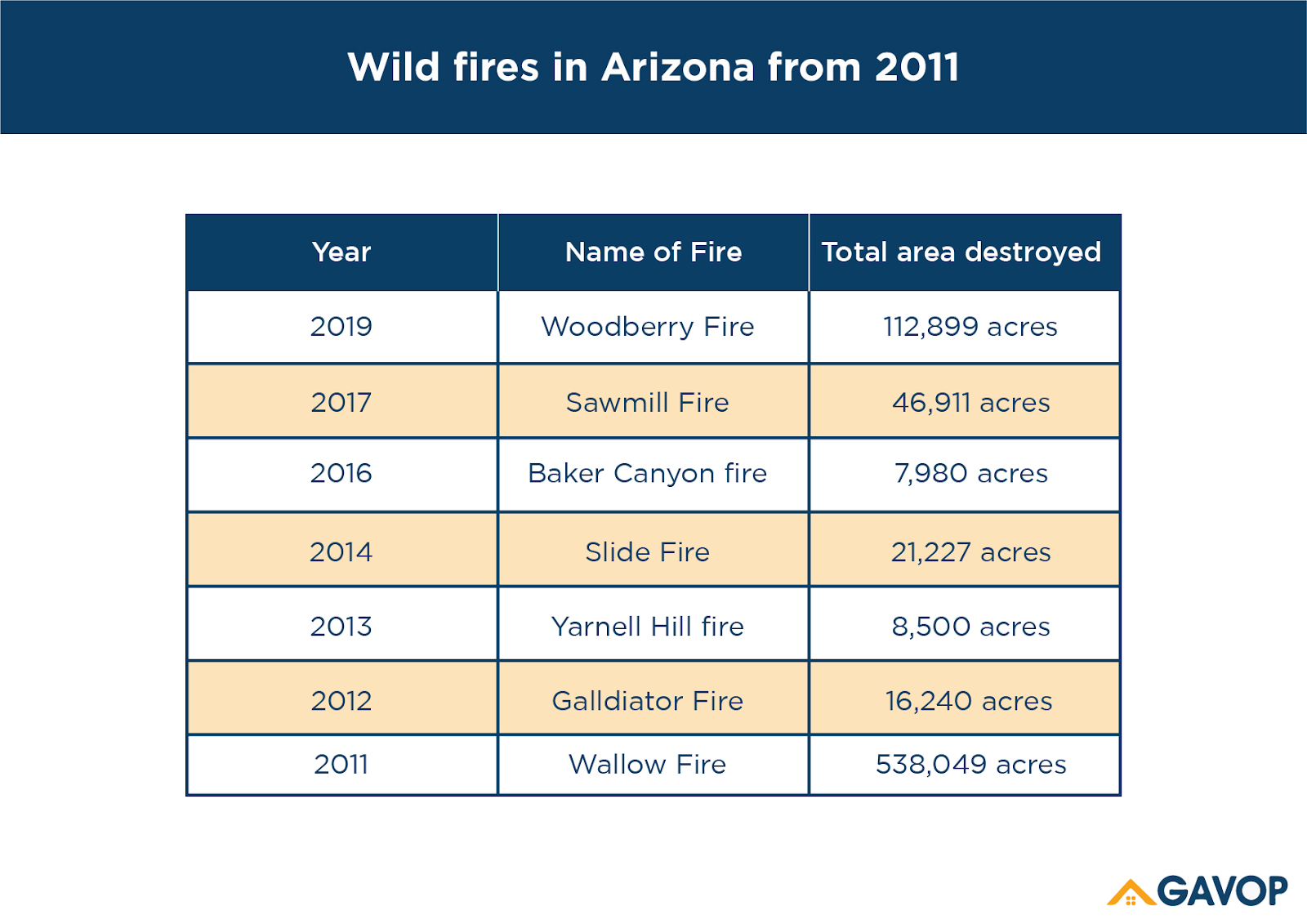

Arizona’s landscape has been dramatically altered because of the rampant wildfires across the state. According to the National Interagency Fire Center, 147,531 acres in Arizona were damaged by wildfires in 2009 alone.Thus, it is wise for homeowners in Arizona to insure their properties against damage caused by wildfires. The following table lists the recent wildfires that have struck Arizona.

In addition to wildfires, flash floods are increasingly common in the state of Arizona. A flash flood could occur within minutes of a cloudburst or a rainstorm. Moreover, because of the altered landscape, both low-lying areas and mountainous regions have become susceptible to flash floods, with water funneling into the canyons from higher grounds.

According to the Arizona Department of Emergency and Military Affairs, only 10% of the flood insurance coverage for the primary structure can be used to repair damages to properties outside the primary structure. To ensure full coverage of accessories outside the primary structure, homeowners must purchase a separate policy for each structure.

Arizona’s Department of Insurance recommends that Additional Living Expense (ALE) is the first type of coverage consumers should enquire about. Under this insurance, reasonable and necessary expenses due to displacement will be incurred by the insurer. Most insurance policies that cover evacuation by authorities include ALE of two weeks. Further, firms generally provide ALE once it is determined that the homeowners are unable to move back to their property because of the damages.

Homeowners can purchase different types of coverage to fully protect their properties.

A dwelling coverage helps pay for any structural damage to the property. Personal property coverage includes damages incurred to property such as furniture and electronics, although items like rare paintings and antiques need to be appraised before their actual value is determined.

Replacement cost coverage covers the present-day cost of property, which is estimated on the basis of a property of equal quality and kind, and it is not subject to deduction or depreciation in the future.

Trees and Shrubs coverage includes the cost of trees and shrubs lost in a fire. Debris Removal coverage covers the cost of removing debris. Automobiles, animals, birds, and fish are generally excluded from a homeowners policy.

ABOUT THE AUTHOR

Ramu Garuda

Ramu is a research analyst with over 9 years of analytics & research experience. Prior to joining the company, he worked with some of the prominent consulting and market research firms in India, including Pride Technology (Supporting consulting projects to PWC), RR Donnelly, and The Hackett Group. His skills include company profiling, benchmarking, data and trend analysis, industry analysis, and report writing across the industries. Ramu holds a Master’s degree in Finance and Marketing. He also has a bachelor’s degree in Biotechnology.