Over 348,000 California Home Insurance Policies Were Not Renewed Citing Wildfire Risk

By: Gokul Menon November, 05, 2019

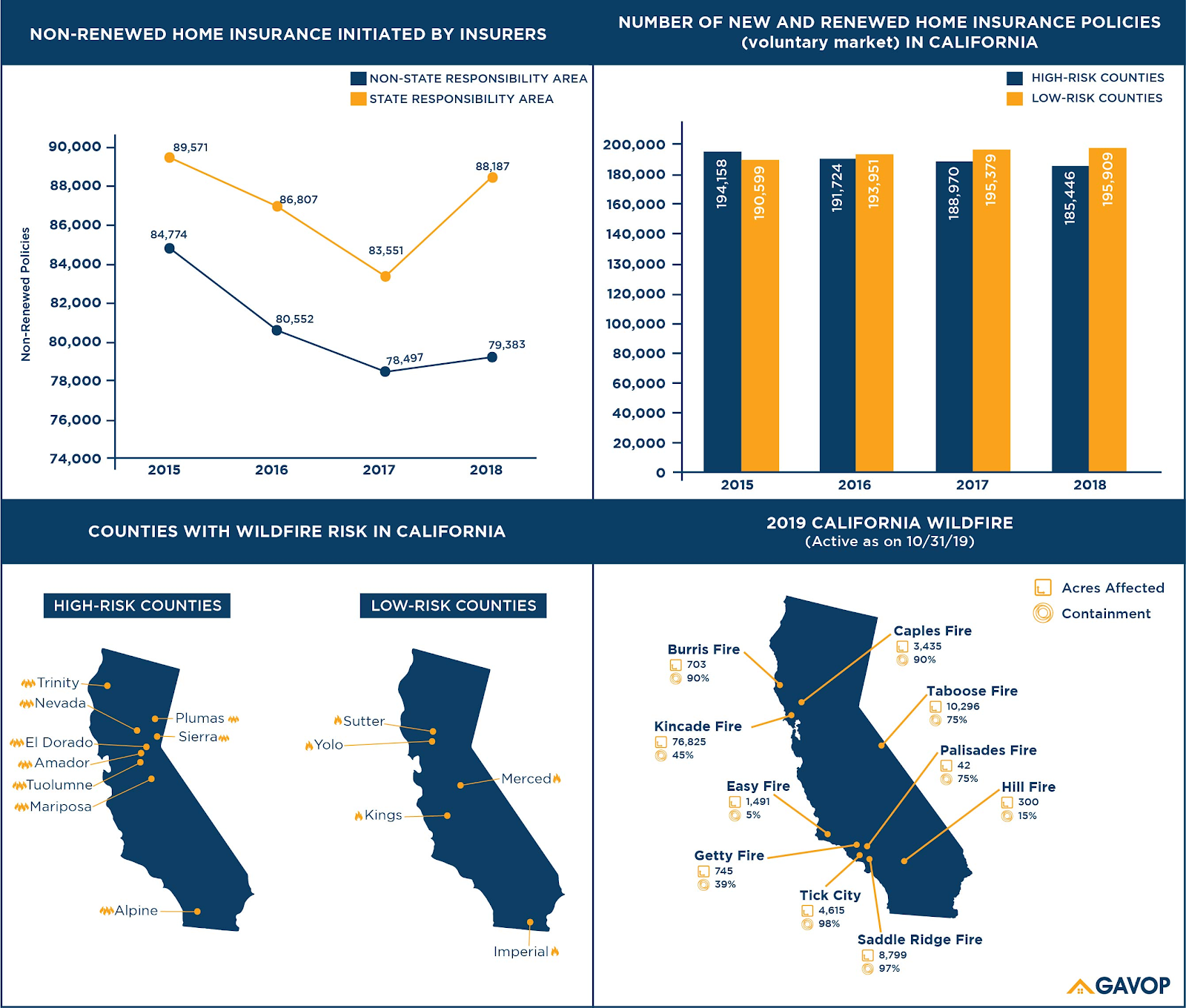

As heavy winds continue to fan flames around Los Angeles, California, finds itself in the middle of yet another wildfire crisis. The last few years have been quite devastating for the residents of California, with repeated wildfires disrupting normal life. Research by Gavop has shown that 348,000 home insurance policies were not renewed due to wildfire risks between 2015 to 2018. Gavop’s research also found a widening gap between non-renewed home insurance policies in state responsibility areas (SRA) and non-state responsibility areas. Non-Renewal saw a record high of 88,187 in 2018 in State Responsibility Areas. This is the highest number of non-renewals between 2016 and 2018. The number of non-renewals by insurers in the voluntary market has seen a steady increase over the last four years. The number of non-renewed policies in State Responsible Areas between 2015 and 2018 amounts to 348,116.

According to the California Department of Forestry and Fire Protection, the 2017 wildfire led to the death of 44 people. And, close to 12,000 structures were lost in this disaster. The wildfire that spread across the state in 2018 was perhaps the deadliest one yet. The flames engulfed over 1,600,000 acres of forest. , and 93 lives were lost in the wildfires of 2018. This year, so far, over 162,000 acres of bushes and forests have been engulfed by flames.

PRESIDENT TRUMP THREATENS TO PULL FEDERAL AID:

Further, President Trump seems to be eager to get into a political tussle, laying the blame completely on the Democratic Governor, Gavin Newsom. He is also threatening to cut federal aid during the time of a disaster that has affected numerous people of California. Trump’s response at the time of such a disaster, has been to blame California’s forest management. California’s Governor shot back with a critique of the President’s environmental policies. The state of California and the President have been at loggerheads in recent times over emission rates.

INSURERS’ RELUCTANCE IN RENEWING HOME INSURANCE POLICIES

Climate Change will become an even more significant influence in the insurance sector in the coming years. As wildfire season gets longer than before, officials lay the blame squarely on climate change. Longer summers seem to be the prime reason for the increase in the size of these fires. Insurance companies now seem to either be playing catch-up to the demands of climate change or are largely ignoring it.

SRAs are areas in which the suppression and prevention of wildfires, is the financial responsibility of the State of California. This covers over 31 million acres in California. The state of California started charging $152.33 since 2014 (SRA Fire Prevention Free) per habitable structure, for structures located in an SRA zone. This fee primarily pays for the different fire prevention services of the SRA. An important part of this service is an attempt to educate householders about fires through public outreach programs. The SRA also spends these funds on mapping and gathering data about wildfire risk-prone areas.

The increasing rate of home insurance premiums for householders in the Golden State adds to the loss and trauma which householders face during such disasters. Consumer Watchdog, a Los Angeles based group, sent an open letter to the insurance commissioner, highlighting the fact that house owners were “unfairly penalized” with exorbitant rates.

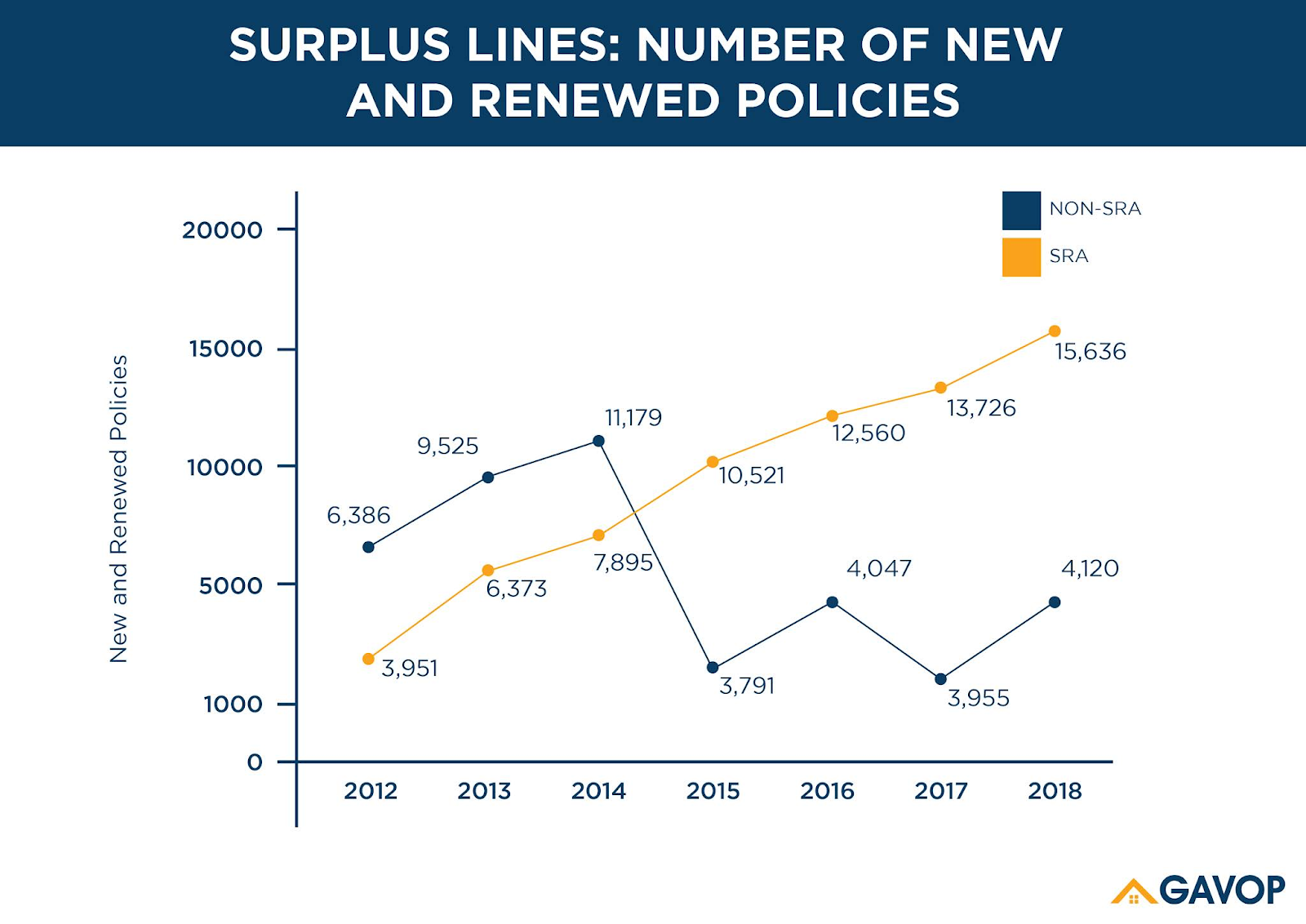

SURPLUS LINES:

The high number of non-renewed insurance policies in the voluntary market means an increasing shift to FAIR Plans and the Surplus Line Insurances. The surplus line market is different since it contains specialized insurers, who cover risks that are not covered by the voluntary market. Surplus lines, in most cases, cannot cover insurances that are being covered by the voluntary market.

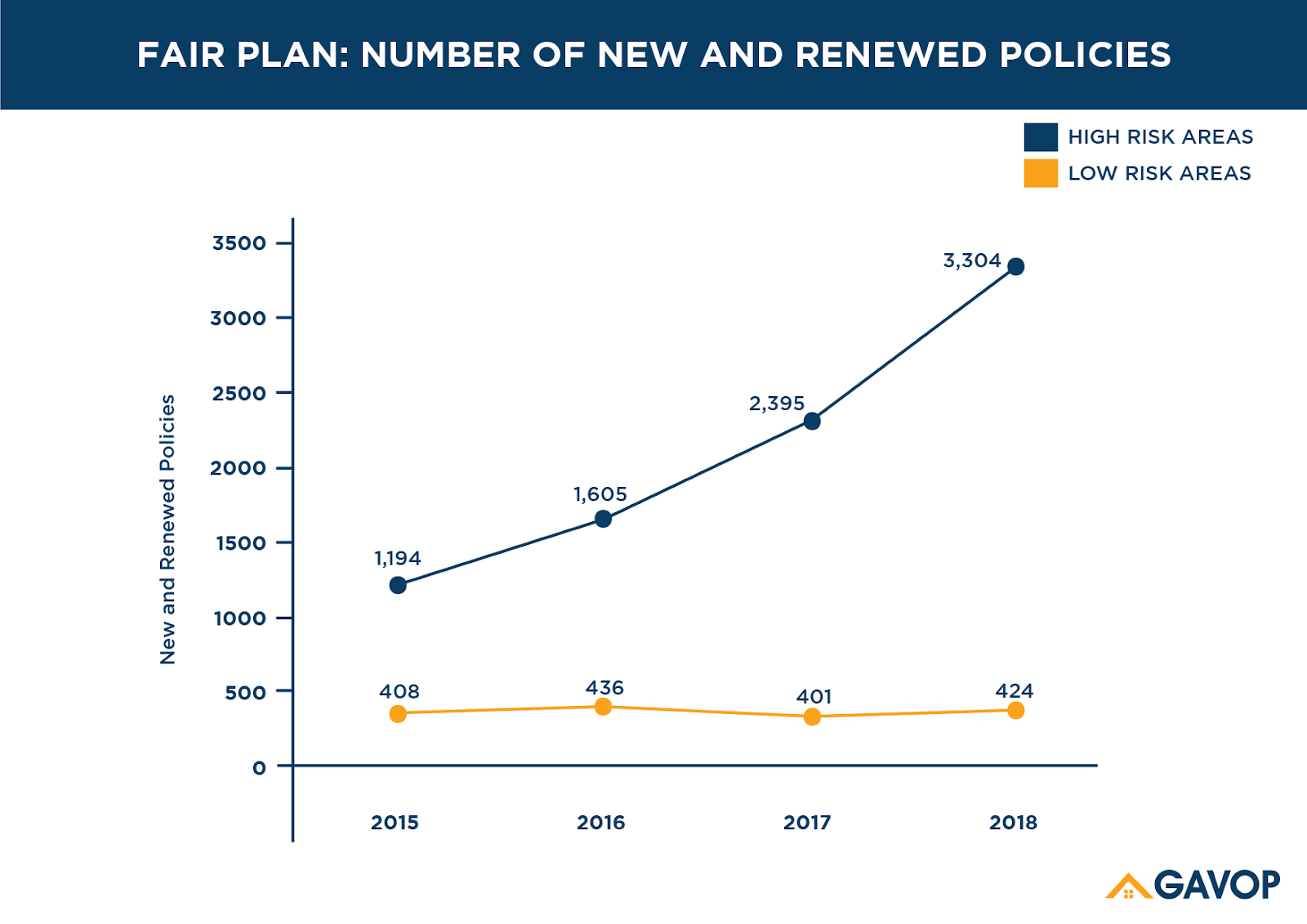

FAIR ACCESS TO INSURANCE REQUIREMENTS (FAIR) PLAN:

This is a state-mandated plan that offers home insurance to homeowners, who are termed “high risk.” This is the last resort for homeowners in high-risk areas, such as the ones mentioned above. We see a substantial increase in the number of renewed and new FAIR Insurance policies in areas that are vulnerable to forest fires. This basic coverage is provided to homeowners at exorbitant rates. The California FAIR Plan Property Insurance suggests that policyholders should check for a different insurer annually.

While the number of new and renewed policies under the FAIR Plan has hovered around the 400 mark in low-risk areas, the numbers have regularly gone up in high-risk areas. From 2017 to 2018, the number of new and renewed home insurance policies under the FAIR Plan saw an increase of 909 policies. This indicates a forced move to more expensive policies because of the lack of options covering higher risk.

PROTECTION FROM WILDFIRE:

Some steps that could be taken to protect one’s house include having closed eaves, rather than open ones, and having dual-pane windows with tempered screens instead of single-pane windows with no screens. Techniques such as controlled burning also seem to be one way of protecting oneself from damage caused by wildfires.

As the fires rage on, let us hope that the burden of higher insurance premiums on householders in high-risk areas lightens.

ABOUT THE AUTHOR

Gokul Menon

Gokul works as a writer at Gavop. He holds an M.A. in Comparative Literature from the University of Hyderabad and a Bachelor’s in English from Madras Christian College. He has been a part of a couple of theatre groups, like Masquerade Youth Theatre and Theatre No. 59 and enjoyed being a part of Literary and Debating circles in Chennai. Gokul is an avid reader and has presented a few academic papers. He spends more time on Goodreads, than on any other social media platform.